The Evolution of Blockchain from Time to Time

People everywhere can now instantly share or communicate information or data with one another over the internet. But, what about transferring money or valuable items?

The transfer of assets or currency at the time being is still very dependent on banks or intermediary institutions. With blockchain, people can securely transfer valuable assets over the internet without duplication or assistance from other parties like banks or other financial institutions.

Blockchain allows ownership and authority over assets (in this case cryptocurrency) to be in the hands of each individual, and this is what makes blockchain technology regarded as one of the greatest innovations of the 21st century.

However, did you know that this technology was actually developed in the 1990s, long before Bitcoin was launched? We will explain the history and the evolution of blockchain, which served as the foundation for the discovery of cryptocurrencies, in this article below.

Article Summary

- 🔗 Blockchain is a technology that allows us to transfer assets that have value over the internet safely without the help of third parties (banks/financial institutions).

- 👨💼Two scientists, Stuart Haber and W. Scott Stornetta, who in 1991 began developing the system that became known to many as blockchain.

- 1️⃣ Bitcoin appeared in 2008 as the first application of blockchain technology. Since Bitcoin was launched, various other applications have been developed which all seek to take advantage of the principles and capabilities of this digital ledger technology.

- 🚀Since the launch of Ethereum with its smart contract technology in 2015, various decentralized applications or dApps (decentralized applications) have been developed, and have increasingly made blockchain integrated with various sectors in the real world.

- 🔎 Blockchain technology is still relatively new and there will be many developments in the future. However, experts currently divide it into three important developments; the launch of Bitcoin, smart contracts, and the adoption of blockchain technology by major institutions.

Blockchain technology is one of the greatest innovations of the 21st century, and its presence has changed the way various sectors work, from finance, gaming to philanthropy. This technology is the foundation that gave birth to the crypto industry.

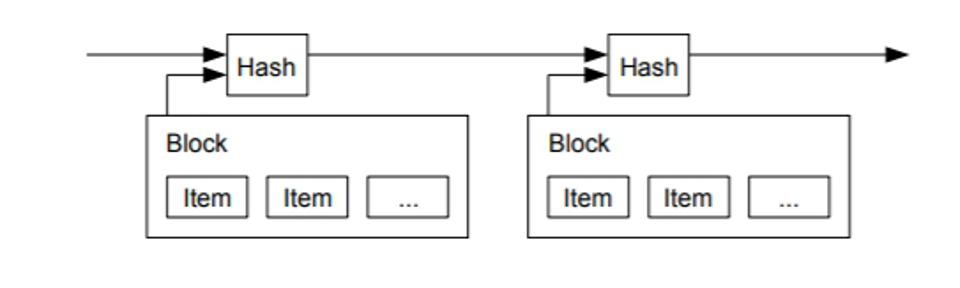

Also known as a digital ledger, a blockchain is basically a collection of blocks containing transaction data that are linked and sequenced with each other to form a chain. The most recent or most recently connected block has the alphanumeric code (hash) of the previous block.

As illustrated above, the hash of each block refers to the hash of the previous block and so on so that the blocks containing transactions form a continuous chain. Therefore, it is almost impossible to modify or tamper with transaction data already recorded on the blockchain, without changing the hashes of previous blocks.

If the transaction data is changed, the hash will automatically change and will change the hash in the next block. This is what makes the blockchain system very safe for recording transactions for sending assets that have value such as Bitcoin.

Early Stages of Blockchain Development

Blockchain technology only began to be known by many people after Bitcoin was launched in 2009. Not many know that this technology has actually been developed since the early 1990s.

💡 It was two scientists, Stuart Haber and W. Scott Stornetta, who in 1991 began developing the system that became known to many as blockchain. Their first work involved working on cryptographically secured blockchains where none existed. which can damage the timestamps of documents that have been recorded.

In 1992, Haber and Stornetta improved their system to combine Merkle Tree with the technology they developed, thereby increasing the efficiency of allowing more documents to be collected on a single block.

Starting from 2008, blockchain started to get a lot of attention, thanks to the work of one person or group named Satoshi Nakamoto who is accredited as the brain behind Bitcoin blockchain technology.

Nakamoto first conceptualized the blockchain of Bitcoin in 2008 and released the first whitepaper on this technology in 2009. In the whitepaper, Nakamoto cites three research results by cryptographers Haber and Stornetta, and provides an explanation of how this technology can be used. increase trust in digital currency delivery with its decentralized aspect.

Blockchain 1.0 – Blockchain First Generation

Blockchain 1.0 is the first evolutionary phase of the blockchain technology. With the introduction of fully decentralized, distributed, and immutable online transaction records, Blockchain 1.0 aims to bring transparency and public access to the global financial system.

Blockchain 1.0 was initiated by Bitcoin which was introduced in 2008. As previously explained, Satoshi Nakamoto in his whitepaper details it as an electronic peer-to-peer system. Nakamoto formed the genesis block (the first block in the Bitcoin blockchain), where subsequent blocks are linked and interconnected resulting in one of the largest blockchains containing various information and transactions.

The launch of Bitcoin made it possible for the first time to execute financial transactions using the blockchain. Bitcoin became known as the “Internet of Money”.

💡 May 22 is observed as Bitcoin Pizza Day, to commemorate the event of the first cryptocurrrency transaction with physical goods. On May 22, 2010, a young man in Florida paid for two pizzas with a certain amount of Bitcoin.

What makes this story legendary is that the amount of Bitcoin paid was 10,000 Bitcoin, which today is worth more than 3 trillion rupiah, for two pizza pans! Since then, the International crypto community has celebrated May 22 as Bitcoin Pizza Day.

Blockchain 2.0: Smart Contract

Bitcoin is known as the first generation blockchain designed to prioritize the security of digital asset transfers. So the programming language on blockchain Bitcoin is not flexible enough for developers to make complex applications on it.

Vitalik Buterin, a programmer who has been involved in the Bitcoin community since 2011 then started working on a blockchain that not only has a function other than being a peer-to-peer network like Bitcoin, but is Turing-complete, or a decentralized computing platform that can run any application.

Ethereum was then officially launched in 2013 as a public blockchain with smart contract functionality, or code that can be programmed for anything. The launch of Ethereum was an important moment in the history of blockchain.

Blockchain Ethereum has developed into one of the largest applications of blockchain technology with smart contract technology which is used to develop various decentralized applications or dApps (decentralized application), and became the beginning of the rapid development of cryptocurrency.

💡 Ethereum is one of the busiest blockchains, following the increasing use of DeFi since 2020 as well as NFT boom since 2021. As of August 2022, total value locked (TVL) in Ethereum blockchain reached 39.97 billion US dollars, or controls 58% market share of the DeFi industry.

Also read: What is Ethereum?

Blockchain 3.0 – Adoption of Blockchain and Crypto by Major Institutions

The history and evolution of blockchain does not stop at Bitcoin, Ethereum and the development of various smart contract platforms. We are now entering the third stage of the development of blockchain technology.

This third phase of blockchain development basically aims to solve the problems that exist in the first and second generation blockchain industry, namely scalability. To facilitate even greater adoption, greater transaction processing capabilities are required, which Bitcoin and Ethereum (before the Merge) had not yet facilitated.

For example, Bitcoin can process 3 to 7 transactions per second, while Visa’s transaction speed is around 2,000 TPS. To be used by more people, scalability certainly needs to be improved.

Some blockchain such as Polkadot, Cardano as well as Ethereum 2.0 or the Merge, are currently being developed to solve the scalability issues that exist in the blockchain previous generations.

This phase will see more and more large companies and institutions adopting blockchain. At this stage, blockchain technology will be widely accepted as the industry standard of how a company or an institution conducts their financial operations and this technology will increasingly enter our daily lives.

💡 One example of the development of blockchain in Indonesia is Bank Indonesia’s plan to start developing a CBDC or Central Bank Digital Currency which is a digital version of the official currency issued by the government to facilitate digital transactions and increase financial inclusion. CBDC is similar to cryptocurrency and operates using a digital ledger to speed up and increase the security of digital transaction processes.

Share