The Future of Stablecoins in 2026: Latest Marketcap and Regulatory Data

Stablecoins are already the backbone connecting the traditional financial system with the digital economy. To understand the future of stablecoins in 2026, this article will further discuss what stablecoins are, their development trends, the latest stablecoin market cap data, the current regulatory landscape, and a direct comparison between stablecoins and Indonesia’s CBDC (Digital Rupiah)!

Article Summary

- 📈 Global stablecoin market cap reached $302.93 billion as of April 2026, led by USDT ($186.9 billion).

- 💸 Monthly transfer volume crossed $10.22 trillion with a total of 243.83 million asset holders.

- 🎯 Stablecoins are predicted to account for 5-20% of the cross-border payments market.

- 🏢 The B2B sector dominates 60% of stablecoin functional usage, driving global transaction volume to $28 trillion.

- 🏦 77% of users prefer official institutional wallets, boosting the value of tokenized assets (RWA) to $27.5 billion.

What is the potential of stablecoins in the future?

Stablecoins are a type of crypto asset whose value is pegged directly to a relatively stable real-world asset, such as a fiat currency (US Dollar, Rupiah, etc.), gold commodity, or other financial instrument. This pegging system was created to eliminate the extreme price fluctuations that are common in pure cryptocurrencies like Bitcoin or Ethereum. For example, a US Dollar-based stablecoin such as USDC or USDT will always be held at approximately the same value as $1.

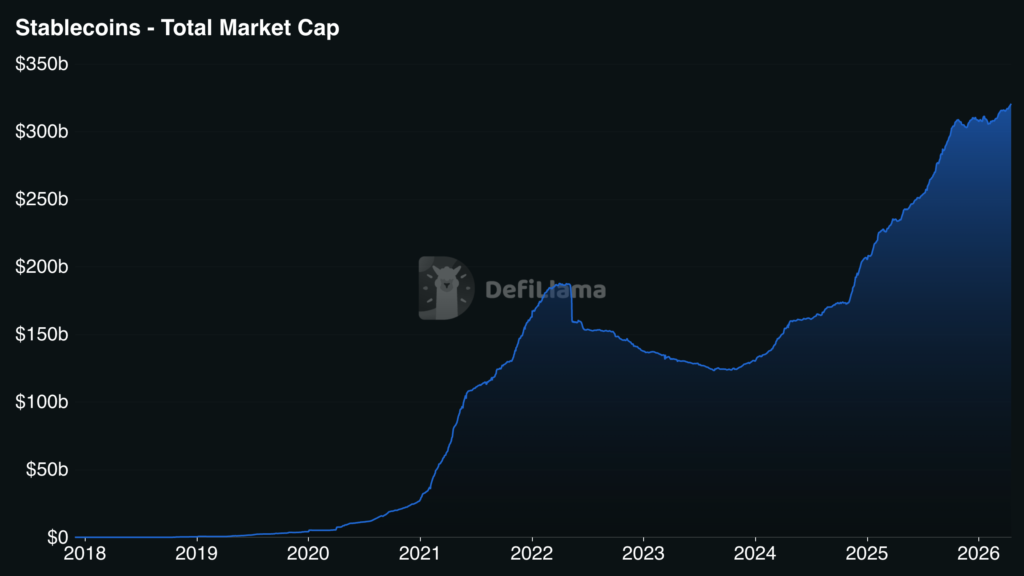

As of April 17, 2026, the stablecoin market capitalization grew rapidly from 2018 to 2026. After peaking at around $180 billion in early 2022 and dropping to $120 billion in 2024, the market took off again and managed to set a new record high of over $300 billion in 2026.

The main objective of this innovation is to combine the stability of conventional asset values with the sophistication of blockchain technology. Through this combination, users can enjoy a financial infrastructure of the future that allows cross-border transactions to be instantaneous, transparent, and fully operational 24/7 without time constraints or geographical barriers. This emphasizes the bright prospects of stablecoins and their role in the crypto ecosystem as an anchor of market stability amid volatility.

Cross-Border Payments

By 2026, the progression of stablecoins from a trading tool to a payment infrastructure is well underway thanks to regulatory support and major investments, such as Mastercard’s acquisition of BVNK. Although the share of usage is still below 1% globally, the market potential is massive, reaching $17.9 trillion, especially in developing regions.

According to Forbes, for legal compliance and risk reasons, many companies prefer to use stablecoin infrastructure for global remittances without directly storing the digital assets. Currently, the strongest adoption is in the B2B payments sector (such as logistics and payroll) as well as dollar digital wallets to hedge against local currency fluctuations in developing countries.

According to a prediction by Eric Barbier, CEO at Triple-A, stablecoins are not expected to replace giants like Visa or Swift, but will take a 5-20% share of the cross-border payments market. While the potential is great for e-commerce andmicropayments, the industry still has to solve obstacles related torecurring payments and app-friendliness to make stablecoins as a digital payment tool usable by the general public.

Full Integration of Stablecoins with Traditional Finance (TradFi)

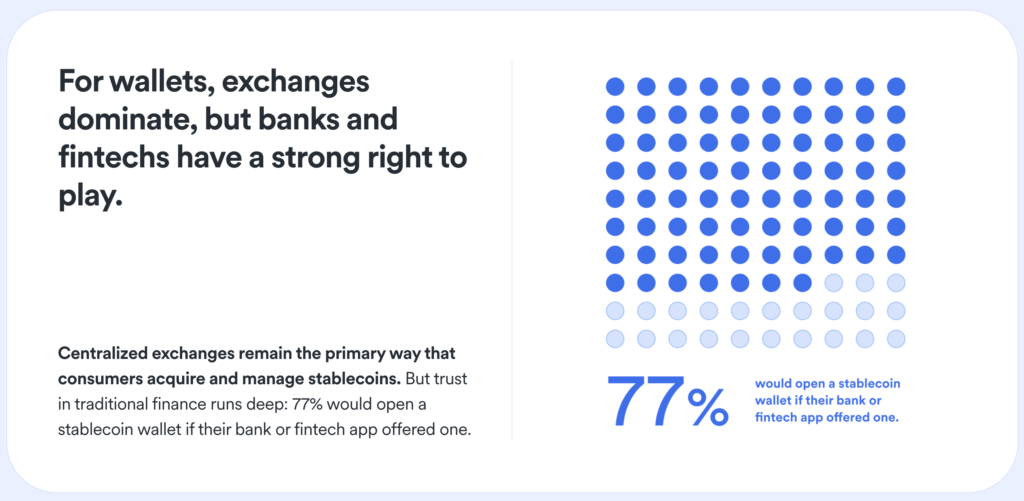

The boundaries between traditional banking and blockchain are fading as trust in financial institutions grows, supported by the widespread use of stablecoins in the fintech sector. Data for 2026 shows 77% of users prefer a stablecoin wallet from a bank or authorized fintech, triggering mega-acquisitions like Mastercard’s $1.8 billion purchase of BVNK.

In response, banks began issuing tokenized deposits-digital assetson the blockchain that remained officially insured. This innovation pushed the value of tokenized Real-World Assets (RWA) to soar to $27.5 billion by early 2026.

This integration greatly benefits cross-border corporate (B2B) transactions by making them faster and cheaper. Today, the B2B sector dominates 60% of stablecoin functional usage and has driven a record $28 trillion in global organic transaction volume, proving that conventional and digital currencies are now merging into one ecosystem.

Latest Stablecoin Marketcap Data in 2026

According to the stablecoin metrics dashboard, the market ecosystem is showing strong growth figures on various key indicators. Here is a breakdown of the data recorded as of April 16, 2026:

- Market Cap: Reached $302.93 billion, with a slight increase of 0.27% compared to the previous 30 days.

- Monthly Transfer Volume: Shows massive transaction activity, touching $10.22 trillion (up 7.20% in the last 30 days).

- Monthly Active Addresses: There were 55.84 million active wallet addresses, registering a significant jump of 14.67% from the previous month.

- TotalHolders: Reached 243.83 million users, up 2.60% in the 30-day period.

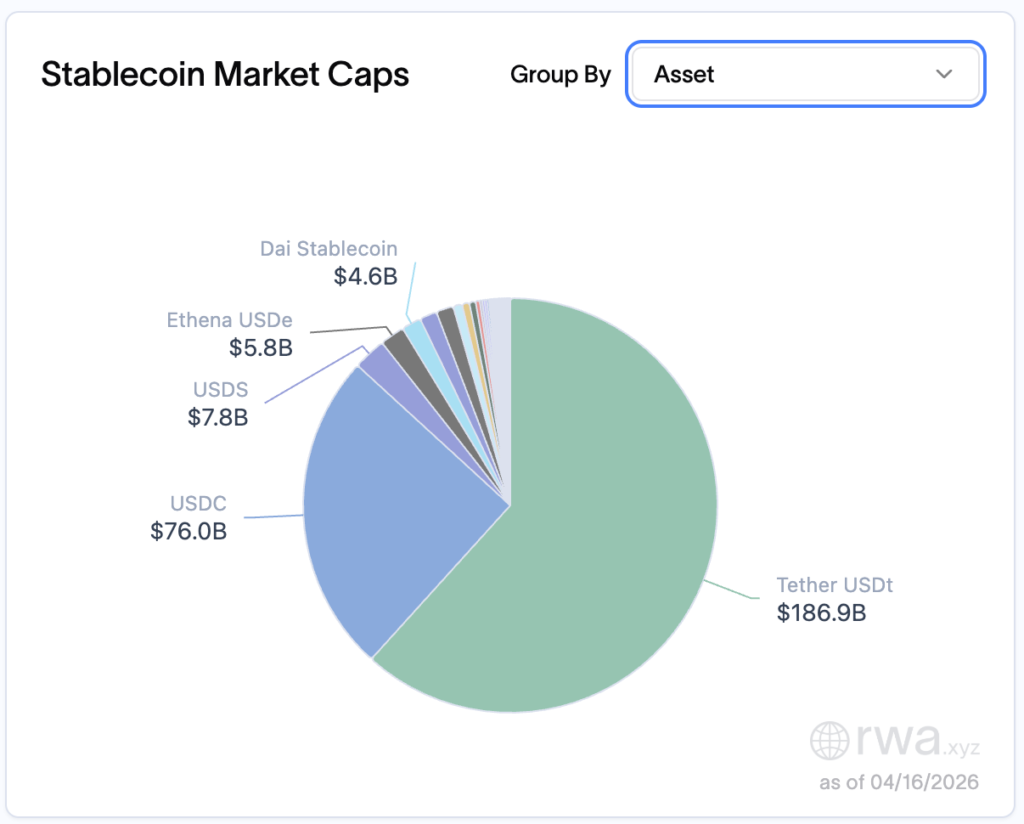

Top 5 Stablecoins by Market Cap

Based on data as of April 16, 2026, the market landscape is dominated by five major assets that are now recognized as the most popular stablecoins in 2026. Tether leads the way at number one with a massive market capitalization of $186.9 billion, followed by USD Coin in second place with a market value of $76 billion.

Rounding out the top five list is Sky Dollar (USDS) in third place at $7.8 billion, followed by Ethena USDe (USDe) at $5.8 billion, and Dai (DAI) in fifth place with a market capitalization of $4.6 billion.

Stablecoin Regulation in Different Countries

Entering the second quarter of 2026, the 2026 stablecoin regulatory landscape at the global level has shifted from the discourse phase to strict enforcement. This is done to minimize the risks of stablecoin regulation that financial institutions have been concerned about. Below is a detailed summary of the regulatory status in key jurisdictions:

Indonesia: The Era of OJK Supervision

As of January 2026, the transition period from Bappebti to the Financial Services Authority (OJK) has officially ended as mandated by the P2SK Law.

- Classification: Stablecoins are no longer seen as a commodity, but rather part of IAKD (Financial Sector Technology Innovation, Digital Financial Assets and Crypto Assets).

- Foundation of Tokenization (POJK No. 27 of 2024): Reinforcing the classification, this regulation becomes the main legal umbrella for the trading of Digital Financial Assets. It sets strict standards for the tokenization process (including stablecoins as a representation of digital fiat). It requires transparency of underlying assets and risk management governance to ensure tokenized products have consumer protections equivalent to traditional financial instruments.

- Mechanism: OJK is implementing a stricter regulatory sandbox. Local stablecoin issuers are required to have a 1:1 reserve that is audited in real-time and held at a domestic custodian bank registered with OJK.

- Focus 2026: Integration of stablecoins for retail payment systems (via synchronized QRIS) is in a limited trial phase to support digital economy efficiency.

United States: GENIUS Act 2025/2026

After years of debate, the US finally passed the GENIUS Act(Guiding and Establishing National Innovation for U.S. Stablecoins Act) in July 2025, which is now the operational standard in 2026.

- Federal License: This law allows non-bank companies to obtain a special federal charter to issue “Payment Stablecoins”.

- Reserve Standard: Requires reserve assets to be cash or short-term T-bills. Algorithmic stablecoins are strictly prohibited from being used as public tender.

- Compliance: As of April 2026, FinCEN and OFAC require issuers to implement automated transaction scanning systems to prevent illicit financing, bringing stablecoin standards in line with traditional banking institutions.

EU: Full Implementation of MiCA

Markets in Crypto-Assets (MiCA) is now the most mature framework in the world.

- Deadline July 2026: The final transition period ends on July 1, 2026. Companies that do not meet MiCA reserve governance and transparency standards are prohibited from operating in the Eurozone.

- Market Impact: Due to highly stringent regulations, some major stablecoins such as USDT (Tether) have been delisted from major exchanges in Europe (such as Binance EEA and Coinbase EU) for failing to meet Electronic Money Institution (EMI) license requirements.

- Consumer Protection: MiCA mandates instantredemption rights for coin holders and prohibits the charging of interest on stablecoins to prevent them from being misrepresented as securities investments.

Hong Kong: Asia’s Stablecoin Center

Hong Kong has become a leader in Asia with a new licensing regime in place since August 2025.

- Banking License: In April 2026, Hong Kong officially issued the first stablecoin license to major institutions such as HSBC and the Standard Chartered consortium.

- Fiat-Backed Focus: The primary focus will be stablecoins pegged to the Hong Kong Dollar (HKDR) to facilitatecross-border trading and settlement of institutional digital asset transactions.

Regulation Comparison Table 2026

| Region | Key Regulations | Status 2026 | Main Requirements Backup |

|---|---|---|---|

| Indonesia | P2SK Law / OJK Rules | Full OJK Supervision | 1:1 at Local Custodian Bank |

| United States of America | GENIUS Act | Federal Operations | Cash & Treasury Bills (T-Bills) |

| European Union | MiCA | Full Implementation | EMI License & Strict Audit |

| Hong Kong | HKMA Licensing | Institutional/Retail | Fiat-backed (HKD/USD) |

Difference between Electronic Money and Digital Money

Digital Money is a form of currency that exists only in electronic format and has no physical form (such as paper or coins). As of 2026, the term specifically refers to money issued directly by central banks or through blockchain technology.

Unlike e-money, which is a digital representation of cash held in banks, digital money is a direct liability of the issuer (such as a Central Bank). Digital money enables direct peer-to-peer (P2P) transactions without having to always go through the cumbersome traditional banking clearing system.

Example of Digital Money in Indonesia

In 2026, Indonesia’s digital finance landscape is no longer just a trend, but the backbone of the national economy. The integration of legal instruments from the central bank, regulated cryptocurrencies, and private digital wallets has created a highly fluid ecosystem.

Rupiah Digital (Project Garuda)

As a Central Bank Digital Currency (CBDC), Rupiah Digital is the only digital payment instrument that is a direct monetary obligation of Bank Indonesia (BI).

- Wholesale CBDC (w-Digital Rupiah): Limited use for settlement of interbank transactions, money market, andtokenized assets transactions. It cuts settlement time from hours to seconds.

- Retail CBDC (r-Digital Rupiah): In 2026, people will be able to access Digital Rupiah through a licensed Digital Wallet application. The main advantage is Programmability; the government can distribute subsidies or social assistance (Bansos) that are “programmed” to only be spent on certain commodities (such as staples or education).

- Offline Functionality: One of the most anticipated features in 2026 is the ability for peer-to-peer transactions without an internet connection (using NFC or Bluetooth technology), especially useful for 3T (Frontier, Outermost, Disadvantaged) regions.

Rupiah Stablecoins (IDRX & IDRT)

- IDRX: Established in 2023, IDRX is a digital asset infrastructure that pegs its value 1:1 to the Rupiah to support the Web3 ecosystem in Indonesia. The instrument prioritizes transaction speed and transparency to connect the national currency with Real World Assets (RWA), with a strategic focus on regulatory compliance and inclusive financial technology development.

- IDRT (Rupiah Token): The first Rupiah-backed stablecoin issued by PT Rupiah Token Indonesia. 1 IDRT is equivalent to 1 Rupiah.

Examples of Electronic Money (E-Money) in Indonesia

In the classification of payment systems in Indonesia as of 2026, Electronic Money (E-Money) is broadly divided into two main categories based on its storage media. Here are the details:

Chip-Based E-Money

Balances are physically stored in the chip on the card. No internet connection is required during transactions(offline), making it very fast for high mobility.

- Prime Examples: Flazz (BCA), e-Money (Mandiri), TapCash (BNI), and Brizzi (BRI).

- Uses: Payment for tolls, parking, and public transportation (KRL, MRT, LRT).

- Characteristics: Anonymous (unless registered) and the balance is lost if the card is lost.

Server-Based E-Money

Balances are stored on the service provider company’s server. Transactions are done online through a mobile application with central database verification.

- Prime Examples: GoPay, OVO, Dana, ShopeePay, and LinkAja.

- Uses: QRIS transactions, e-commerce shopping, and bill payments (electricity, credit, insurance).

- Characteristics: Requires internet access and has layered security (PIN/Biometric).

Stablecoins vs CBDC Indonesia: How Are Things Going?

| Criteria | Stablecoins (e.g. USDT, USDC) | CBDC (Rupiah Digital / Garuda Project) |

|---|---|---|

| Publisher | Global private companies (such as Tether or Circle). | Bank Indonesia (BI). |

| Legal Status | Recognized as crypto assets/commodities (regulated by Bappebti/OJK), prohibited as domestic payment instruments. | The country’s official digital currency(legal tender). |

| Infrastructure | Global public blockchain (open, without national borders). | A centralized private network that is fully controlled by Bank Indonesia. |

| Usage Focus | Investment,hedging against Rupiah fluctuations, and global funds transfer (DeFi/Web3). | Efficiency of interbank transaction settlement(wholesale) and national payment system integration. |

| Main Pros | Massive global liquidity and direct access to the US dollar financial ecosystem. | It is 100% guaranteed by the state, free of default risk, and maintains Indonesia’s monetary sovereignty. |

Looking to the future of stablecoins 2026, In Indonesia, Digital Rupiah (Project Garuda) and stablecoins will complement each other. Bank Indonesia is focusing on Digital Rupiah for the efficiency of large-scale (wholesale) interbank transactions to maintain monetary sovereignty. On the other hand, as pure cryptocurrencies are banned as domestic payment instruments, international citizens and businesses will continue to utilize stablecoins for cross-border merchant payments, remittances, and access to the Web3 ecosystem.

The challenge and opportunity ahead is to establish interoperability between the Rupiah Digital closed system and the stablecoin public blockchain network, in line with the P2SK Law. This integration will create a hybrid financial ecosystem: Digital Rupiah secures the domestic economy, while stablecoins accelerate cross-border business exchanges (such as export-import) with global liquidity.

Conclusion

By 2026, stablecoins will have evolved from a hedge to a global payment infrastructure that is integrated with traditional banking thanks to mature regulations (such as OJK and MiCA). These instruments will not replace Central Bank Digital Currency (CBDC) such as Digital Rupiah, but rather complement each other: CBDCs focus on domestic economic efficiency and sovereignty, while stablecoins facilitate cross-border transaction liquidity in a fast, cheap and transparent manner.

How to Buy Stablecoins on the Pintu?

On Pintu, stablecoin purchases can start with a very affordable amount, starting from Rp11,000. Here’s how easy it is to buy stablecoins on Pintu:

- Enter the Pintu homepage.

- Go to the Market page .

- Search and select a crypto asset in the Stablecoins category .

- Enter the amount you wish to purchase, and follow the rest of the steps.

FAQ

Can stablecoins be used as payment?

It can; it is now a payment standard where JPMorgan does instant settlement, Mastercard integrates it into its global network, and BlackRock provides real-time liquidity through the BUIDL tokenized fund.

What are the Top 5 Stablecoins Right Now?

The current market dominance is held by Tether (USDT) as the liquidity leader, the regulatory-compliant USD Coin (USDC), Ethena (USDe) with its synthetic yield feature, the decentralized USDS (an evolution of DAI), as well as the fast-growing USD1 from the World Liberty Financial ecosystem.

What is the Potential of Stablecoins as Investment Assets?

While the value is fixed, the investment potential lies in earning yield (interest) through DeFi protocols or lending platforms that often exceed traditional bank rates, as well as its function as a safe hedging instrument against local currency inflation.

Which is Safer, Stablecoins vs Bitcoin?

The safety of both depends on the type of risk: Stablecoins are safer from price fluctuations but come with the risk of centralization and asset backup, while Bitcoin is much more volatile but is considered more fundamentally secure due to its decentralized nature and cannot be frozen by any party.

Reference:

- https://defillama.com/stablecoins

- Chainlink. CBDC vs. Stablecoins: The Battle for the Future of Money. Accessed April 16, 2026

- Forbes. Stablecoin Cross-Border Payments In 2026: From Theory To Practice. Accessed April 16, 2026

- BVNK. Stablecoin Utility Report 2026. Accessed April 16, 2026

Share

Table of contents

Related Article

See Assets in This Article

USDT Price (24 Hours)

Market Capitalization

-

Global Volume (24 Hours)

-

Circulating Supply

-